De-dollarization is the process of countries slowly moving away from using the US dollar. Two ways they do it, via central banks reducing their US dollar reserves in favor of gold and other major currencies, and using currencies other than the US dollar to settle some international payments in trade, tourism and so on.

Since around the middle of 2022, the term “de-dollarization” has been cropping up more often. For instance, here are some reports and opinion pieces that came out this month: “US dollar’s decline could benefit Asian economies” (Asia Times, Aug. 4), “De-dollarization: Why countries are seeking alternate currencies” (CGTN, Aug. 5), “De-Dollarization: What Is It, and Is It Happening?” (Investopedia, Aug. 16), “The Real Cost of De-Dollarization” (Project Syndicate, Aug. 16), “China urges BRICS to become geopolitical rival to G7” (Financial Times, Aug. 21), “Is the dollar finally on its way out?” (East Asia Forum, Aug. 21), “De-dollarization is irreversible — Putin” (RT, Aug. 22), “Trends, Reasons and Prospects of De-dollarization” (South Center, August 2023).

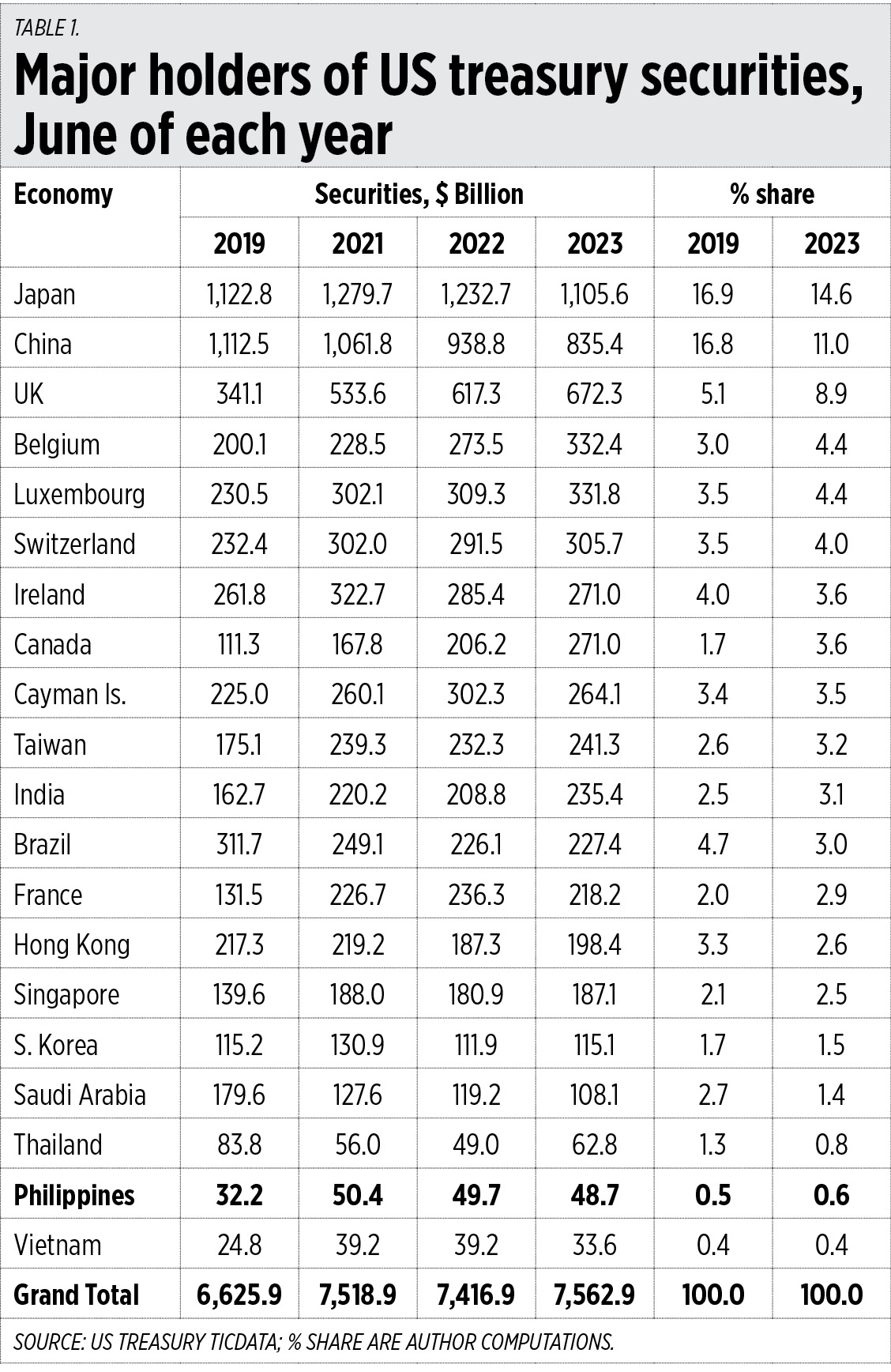

To see how valid this observation or process is, I checked the country origin of US treasury securities — the total has increased from $6.626 trillion in June 2019 to $7.563 trillion in June 2023. The biggest lenders to the US government are Japan and China, Japan alone provided 17% of the total in 2019 but this has declined to 14.6% in 2023.

The BRICS (Brazil, Russia, India, China, South Africa) are either reducing their lending to the US, or not lending, or there is no data from them about this (Russia, South Africa). The US has imposed economic sanction against Russia since 2014 when it annexed Crimea, then strengthened the sanctions in 2022. The share of China, India, Brazil, and Hong Kong has declined from 27.3% in 2019 to 19.7% in 2023. Saudi Arabia’s share has declined by half, from 2.7% to 1.4%.

The Philippines, Thailand, and Vietnam also have exposure to US debt but their combined share is small, 2.2% in 2019, down to 1.8% in 2023 (See Table 1).

On Aug. 2, Fitch downgraded its US credit rating from AAA to AA+ mainly due to “the expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance relative to ‘AA’ and ‘AAA’ rated peers over the last two decades that has manifested in repeated debt limit standoffs and last-minute resolutions.”

The world’s big exporters of energy and mineral products include Russia, Qatar, Iran and Iraq. Note that they are non-lenders or minor lenders to the US.

One common narrative during the Russia-Ukraine war is that Russian exports of energy and minerals have declined because of the heavy economic sanctions imposed by the US and NATO allies. This is not true, it is fake news. Russian exports expanded from $249 billion in 2021 to $350 billion in 2022. The Russian market has changed, from its European neighbors to India, China, and Turkey, which refine Russia’s crude oil and export the refined oil products to Russia’s European neighbors. The Europeans now suffer from higher energy prices and higher overall inflation.

But the major winners and gainers from the sanctions against Russia are the US itself, which expanded its LNG exports to Europe, the United Arab Emirates (UAE), whose exports have expanded 5.3 times from 2017 to 2022, Saudi Arabia, Canada, and Norway (See Table 2).

The Philippines, Vietnam, and Thailand remain small players in energy and mining exports. The Philippines has failed to benefit from the higher prices of gold, copper, and silver over the last three years because of our anti-mining policies, especially the anti-open pit mining policies. And we endured high oil-gas prices when we could have a new domestic gas supply aside from Malampaya if the service contract there had been extended much earlier.

The main lesson for the Philippines and other developing countries is that we should reduce our dependence on the US dollar as forex reserves and as currency payment in our trade with other countries. We should have more gold reserves, more yen, yuan, won and other Asian currencies as reserves.

The US credit rating downgrade by Fitch is among the most recent proof of cracks in the US economic and financial power. It has too much public debt, has a high annual budget deficit, has been engaged in many costly and unproductive wars abroad, and is even preparing for a big war with China over Taiwan.

The Philippines needs more trade, more investments, more tourism, more peace based on commerce and not based on missiles. We need more cargo ships, not battle ships. More diplomats and traders, not more generals and admirals.

---------------

See also:

BWorld 630, GDP growth resilience, and the finance and budget lecture at the PDE reunion, August 26, 2023

BWorld 631, Energy realism: Decarbonization and deindustrialization, August 27, 2023

BWorld 632, Financing Growth, August 30, 2023.

No comments:

Post a Comment