* My article in BusinessWorld, January 31, 2022.

------------

— Adam Smith,

The Wealth of Nations (1776), Book IV Chapter VIII, v. ii.

ON Dec. 6, 2021, the Department of Trade and Industry (DTI) imposed an anti-dumping duty on Philippine cement imports from Vietnam at the following rates: Type 1 cement, $1.02 to $10.53 per metric ton (MT) or 2.7% to 31.9% of the export price; and Type 1P cement, $1.16 to $12.79 per MT or 3.8% to 29.2% of export price. DTI estimated that these provisional duties will add P2.01 to P25.08 per 40 kilo bag of cement to the import cost.

Then on Dec. 9, the Tariff Commission (TC) began a formal investigation after it received a request from the DTI and the complete case records. A preliminary conference was held on Dec. 20.

The policy of imposing anti-dumping duty is based on the complaint and lobby by some local cement manufacturers, especially subsidiaries of big multinationals like Lafarge Holcim (Switzerland), CEMEX (Mexico), and CRH (Ireland) that (a.) cement imports from Vietnam are sold here at artificially low, “dumped” prices, (b.) leading to business injuries to local cement manufacturers.

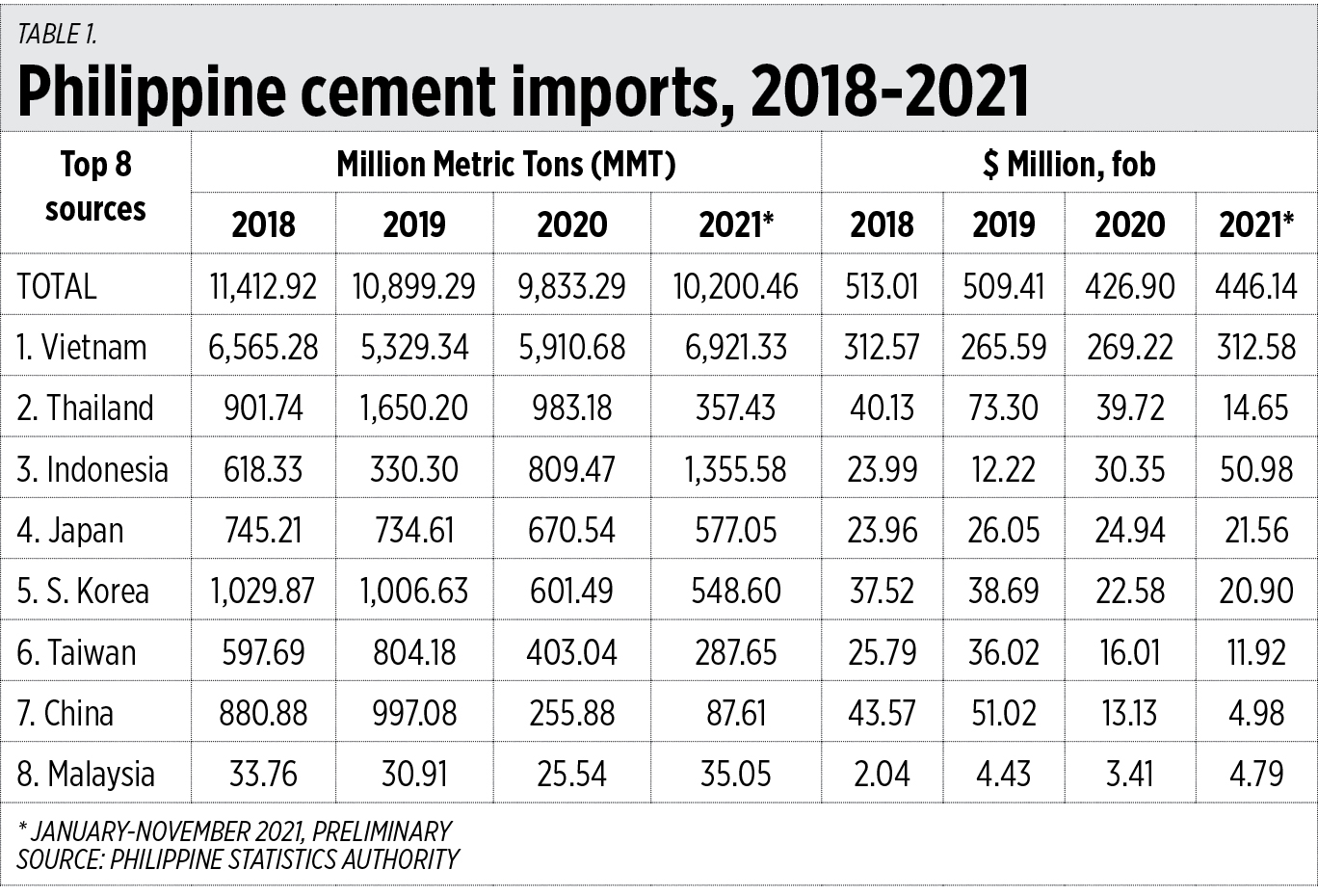

Do these two allegations have a basis? To analyze (a.), I requested data on Philippine cement imports from the Philippine Statistics Authority (PSA), and to analyze (b.), I checked data from the BusinessWorld Top 1,000 Corporations.

The Philippines’ domestic production of 24 to 26 million metric tons (MMT) of cement yearly is insufficient to supply domestic demand of up to 35 MMT. Hence, the Philippines imports 10 to 11 MMT yearly from many countries, some 5 to 7 MMT of which are from Vietnam, another 1.5-2 MMT from Thailand and Indonesia, another 1.2-1.7 MMT from Japan and South Korea.

In terms of value, the Philippines’ cement imports were $427 million to $513 million yearly, free on board (fob). Some $266-$313 million of which are from Vietnam, another $64-$85 million from Thailand and Indonesia (Table 1).

From these numbers, I computed the percent share of these country sources, then divided the value over quantity to get the average price per kilo. Vietnam’s share is 49% to 68% of total imports, followed by 13% to 18% from Thailand and Indonesia.

On imported prices, here is an interesting revelation: the average price is only 4.37 to 4.67 US cents per kilo. And the cheaper cement did not come from Vietnam but from Thailand, Indonesia, South Korea, Japan, and Taiwan (Table 2).

So, why did the local manufacturers, who lobbied for more expensive cement imports via the imposition of an anti-dumping duty, not complain about the much cheaper cement from these five Asian countries?

These prices are equivalent to P2.14 to P2.38 per kilo at P49 to P51 per $1 exchange rate, or P86 to P95 per 40-kilo bag — really cheap. But this is still free on board (fob) value, so there are additional costs to add — shipping, insurance, docking delays (if any), trucking, storage, others. Plus the importers’ and retailers’ profit margin. Perhaps retail prices of P170 to P190 per bag. If so, then consumers benefit if they can save at least P20/bag.

Next test, (b.) — did domestic cement producers really suffer business injuries due to cheap cement imports?

According to the BusinessWorld Top 1,000 Corporations, all these local manufacturers experienced an increase or flat gross revenues in 2019 compared to 2018 except Holcim. The decline in revenues in 2020 was mainly due to the lockdown and pandemic. Even then, some companies experienced increases in net income — Apo, Northern, Philcement. Eagle and Republic Building Materials, Republic Iligan/Mindanao have no data for 2020 (Table 3).

Usually companies drop out of the Top 1,000 in a given year not because they suffered a huge decline in revenues but because they had not yet submitted their financial statements to the Securities and Exchange Commission at the time that the BusinessWorld research department was collating the data.

From the above discussions, we can conclude the following:

One, high cement imports from Vietnam imply their products are cheaper than domestic products, but Vietnam prices are more expensive than cement from Thailand, Indonesia, South Korea, Japan, and Taiwan. But imported cement from these countries were not targeted for anti-dumping duties by the local manufacturers, especially the multinationals.

Two, imposing duties against exports of fellow ASEAN country is not good as we are supposed to have a free trade, zero tariff ASEAN Economic Community (AEC). The lobby for expensive cement imports did not include cement from Thailand and Indonesia because it is not good to expand trade disputes.

Three, data on gross revenues and net income show that there are no clear business injuries for the local manufacturers except for Holcim and Republic Cement. One possible reason is that these two companies have high prices and many consumers have shifted to imported cement.

Four, “dumping” is actually pro-consumer. Households, and commercial and government consumers benefit when cement prices are low and supply is large. Domestic production should expand big time and prices should go down to levels similar to those of imported products.

Five, TC and DTI should not consider making the current provisional anti-dumping duty permanent. The duty should go back to zero. As Adam Smith pointed out, the main goal of production (and trade) is to satisfy the customers.

See also this column’s piece on cement tariffs three years ago, https://www.bworldonline.com/economic-prospects-2019-and-cement-tariff/ (Jan. 24, 2019).

-------------------

See also:

BWorld 524, The transportation sector and the motorcycle taxi, February 01, 2022

BWorld 525, Major power companies, the Indonesia coal export ban, and the PCCI election, February 03, 2022

BWorld 526, Economic stagnation, de-industrialization, and lockdown in the Philippines, February 06, 2022.

No comments:

Post a Comment