The economic impact of 2 years of war in Ukraine, and the Philippines fiscal situation

February 27, 2024 | 12:02 am

My Cup Of Liberty

By Bienvenido S. Oplas, Jr.

https://www.bworldonline.com/opinion/2024/02/27/577880/the-economic-impact-of-2-years-of-war-in-ukraine-and-the-philippines-fiscal-situation/

Last Saturday, Feb. 24, marked the second year of the Russian invasion of Ukraine. Immediately after that, the US and EU allies imposed more economic sanctions against Russia, on top of existing sanctions imposed when Russia annexed Crimea in 2014. The most severe sanction was the freezing, if not confiscation, of Russia’s foreign reserves worth $300 billion.

Important questions to ask: Did those punitive sanctions vs Russia really weaken it? And were those that imposed the sanctions better off?

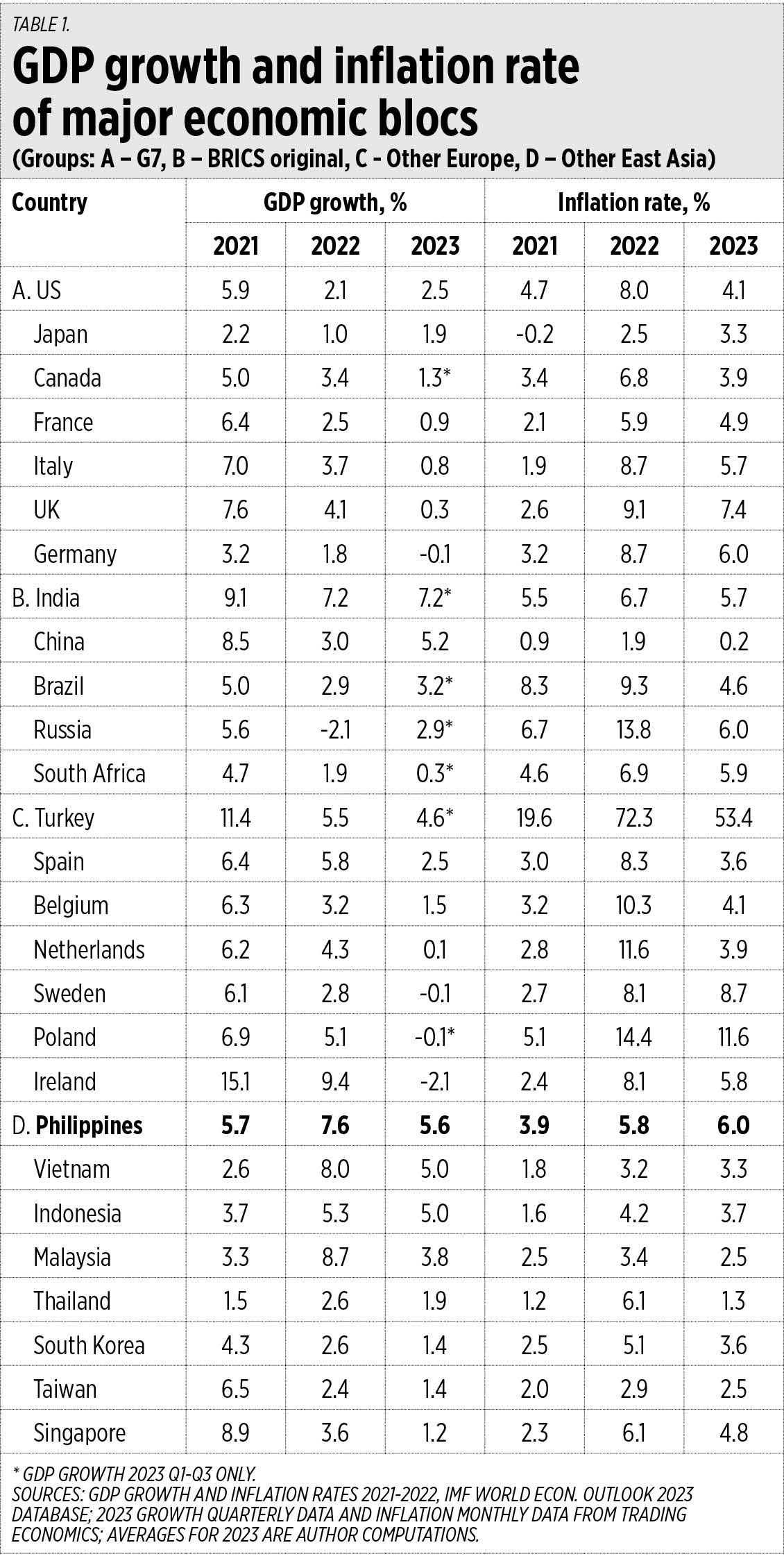

To help answer these questions, I again checked the economic performance of the major players — the US and G7 countries plus other major EU countries on the one hand, and Russia and its economic allies in original BRICS (Brazil, Russia, India, China, South Africa) on the other. I added other East Asian countries to the list to see their performance.

When it comes to GDP growth in 2022 and 2023, all the European countries in the G7 and others in the list suffered consistent growth decline, even contraction (Germany, Sweden, Poland, Ireland), in 2023. In contrast, the BRICS economies retained a path of growth except for South Africa. Russian growth in 2023 was more of a “base effect” from a contraction in 2022.

When it comes to inflation rate, all the G7 and other Europe countries experienced decades-high inflation rates in some months of 2022. These declined a bit in 2023 but still high rates compared to their historical average rates. BRICS, however, just had fluctuating rates from 2021 to 2023. China, meanwhile, is close to deflation.

So back to the original questions. Did those punitive sanctions vs Russia really weaken it? And were those that imposed the sanctions better off?

The answer is “no.” The countries that imposed hard sanctions were the ones that suffered economically via low growth, if not contraction, plus very high inflation. Europe’s industrialization was largely powered by cheap oil and gas from Russia, and when they reduced, if not cut off, such a cheap energy source, they had to source expensive oil/gas from elsewhere.

Meanwhile, the East Asian countries have had a mixed experience — fast growth for the countries with big populations, namely the Philippines, Indonesia, and Vietnam; and growth deceleration for those closely aligned with the US like South Korea, Taiwan, and Singapore (see Table 1).

I asked Budget Secretary Amenah F. Pangandaman and other members of the economic team about the country’s performance. She replied that “the Philippines was able to escape the economic instability suffered by many countries, we even grew fast the past two years — 7.6% in 2022 and 5.6% in 2023. I believe our measures on fiscal consolidation, productive spending for socio-economic development and hard infrastructure via Build Better More, faster implementation of projects, more efficient public spending via digitalization in transactions and open government partnership, have contributed to our economic resiliency and dynamism.”

I think this is a solid assessment. We must just make sure that the big annual budget deficit and public borrowings are controlled so that less public resources are devoted to interest payments.

I also checked the cash operations report (COR) released monthly by the Bureau of the Treasury (BTr), particularly on revenues and how they perform given the huge yearly fiscal gap.

Revenues have recovered and by 2022 were higher than 2019 levels, except when it came to excise tax collections which declined from P318 billion in 2021 to P312 billion in 2022 and P278 billion January-November 2023 (see Table 2).

I asked Finance Secretary Ralph G. Recto about this trend, he said that “Excise taxes on tobacco are falling due to smuggling and illicit trade. When taxes are high, illicit trade and smuggling become very profitable. Furthermore, unregulated disposable vape products are being smuggled as well. I would support banning disposable vape products and penalizing e-commerce platforms selling them, including regulated vape products without stamp (excise) tax.”

Great points, Secretary Recto. I have written at least two pieces in this column about him before: “Senator Recto’s tax cut plan shadows Reagan, Thatcher, and Trump tax cuts” (Nov. 23, 2020), and “Revenue challenges faced by new Finance chief” (Jan. 16, 2024).

In my second article about Mr. Recto, I noted that for 2024, “The BoC may target collecting P1.8 trillion by significantly controlling smuggling and illicit trade. From the estimates Representative Joey Salceda gave last October, tobacco smuggling alone results in about P60 billion/year in revenue losses. The BoC plus other lead enforcement agencies like the Philippine National Police and the Coast Guard should work harder in controlling illicit trade because their annual budgets are huge and come from taxes, so they should strive to control tax leakage.”

The Philippines has gained the economic momentum, growing fast even when many countries were growing slowly if not contracting. Our economic team is composed of seasoned technocrats who have the wisdom to decide when to move forward with economic intervention and when to pull back. Thank you, Sec. Pangandaman, Sec. Recto, and Sec. Arsenio Balisacan.

---------

BWorld 680, The nuclear option to energize growth, Feb. 24, 2024

BWorld 681, Low inflation, low unemployment, high growth — this is the Philippines, Feb. 25, 2024

BWorld 682, The nuclear option for Asian industrialization, Feb. 27, 2024

BWorld 683, NAIA privatization is good, legislated minimum wage is bad

BWorld 684, The nuclear trade mission to Canada

No comments:

Post a Comment