Unlike the markets in the US, Japan, UK, Germany and

other democratic countries, the case of China will always be internally

conflicting. It is a dictatorship that abhors political competition and yet it

wants to mimic economies that allow market competition.

HIGH PUBLIC DEBT

Officially, China has a gross public debt/GDP ratio of

only 41% in 2014, manageable and just slightly higher than the debt/GDP ratio

of Taiwan and South Korea (38% and 36%, respectively). But China has more debt

than what it will officially admit.

A report by McKinsey Global Institute recently said that

China’s total borrowings (individuals + companies + local and central

governments + state enterprises) was 282% of GDP in 2014. This is very high for

a non-industrialized economy like China.

There is high-margin lending (borrowed funds for stocks

investment), reaching $323 billion last month alone, invested in the stock

market by many novice, first-time stock investors numbering in tens of

thousands.

STOCK MARKET

BUBBLE

From 2010-2014, China’s stock market capitalization/GDP

ratio averaged only about 45%. By June 12 this year, it rose to almost 100%,

showing a huge asset price bubble in the first half of this year.

In comparison, this ratio is mildly increasing in the US

(around 140% in 2014) and Japan (nearly 100% in 2014) from 2011 up to the

present.

Figure 1 (from Bloomberg)

The bubble started last year when government media

repeatedly announced that stocks were cheap, with the implicit understanding

that the central planning authorities can control prices from falling. Millions

of novice and first-time stock investors came in droves, China’s market

capitalization tripled and reached $9.8 trillion, according to a Bloomberg

report last June 30.

From 2011 to mid-2014, Shanghai’s price-to-earnings (P/E)

ratio was only around 12. By late 2014-mid-2015, this rose to 26, more than

double in less than one year.

BUBBLE CRASHED

Why did the bubble burst so suddenly? There are several

explanations and hypotheses for this.

One is that China is experiencing a GDP growth slowdown

of “only” 7% or less, compared to 9-12% per year for the last three decades or

more. Two, some government stimulus programs to shield China from various

global turmoil have to end. Three, finance also follows the law of gravity: the

speed and height of price rise is somehow directly proportional to the speed

and depth of price decline.

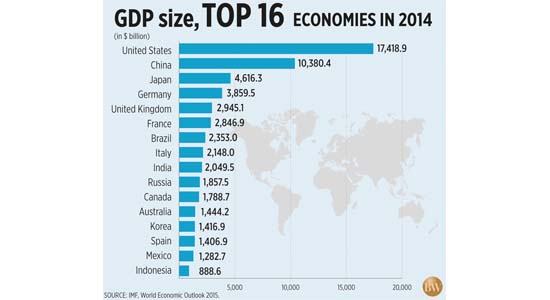

The magnitude of the stock price decline was $3.9

trillion, according to the Bloomberg China Market Cap index. That was

equivalent to the GDP size of Germany, larger than the GDP sizes of UK or

France or Brazil, and twice the GDP of Russia.

Figure 2.

The bulk of China stock investors are the more than 90

million individuals who make up about 80% of the market, according to a survey

of households.

The stocks crash was worse than the US property crisis in

2008-09, although in terms of global interconnection and contagion, the US

financial turmoil last decade had a larger impact. Significant deterioration in

the public debt of Greece, Spain, Portugal, Ireland, Cyprus, Italy, etc.

occurred in 2009 and 2010, obviously a result of contagion from the US.

Compared to the Greece debt problem, this is much larger.

Greece’s GDP size in 2014 was only $238 billion, and its total public debt was

about $320 billion.

CENTRAL PLANNING

FIGHTS BACK

China’s government responded with several measures. One,

the central bank cut interest rates, hoping that more savings from the banks

will go to the stocks market. Two, some stock traders and speculators were

investigated with threats of prosecution for stock rumor mongering. Three, a

number of planned initial public offerings (IPOs) were suspended. Four,

outright stop in trading.

From Bloomberg reports:

“At least 1,301 companies have halted trading on mainland

Chinese exchanges, locking up $2.6 trillion of shares, or about 40 percent of

China’s market capitalization. The China Financial Futures Exchange raised

margin requirements for sell orders on CSI 500 index futures, while the central

bank will provide “ample liquidity” to the stock market. China Securities

Finance Corp. said it will buy more shares of small- and mid-cap companies.”

(July 8)

“Official measures to support shares became more extreme

during the week as declines deepened. They include a ban on stockholders and

executives from selling stakes in listed companies for six months, an order for

companies to buy equities and an investigation by the nation’s public security

bureau into short-selling.” (July 10)

LESSONS FOR

SOUTHEAST ASIA

Emerging economies in the region like the Philippines can

draw lessons from this latest episode in regional and global economics.

1 Moral hazards. When a central planning government

rallied the public to invest in the market, many investors with little or zero

experience in the market came believing they couldn’t lose money since the

government is big enough to guarantee returns or bail them out later.

2 Adverse selection. Millions of new novice investors

have picked up the wrong timing, at a time when fiscal uncertainty hounds the

EU and China was experiencing growth slowdown. Adverse selection often results

in adverse results.

3 Debts and uncertainty. As public and private debts

become bigger and bigger, the economic uncertainty also becomes bigger. People

will never know who can pay back and when, and who will default.

4 Corporate fundamentals. Investors should do hard

analyses of the fundamentals of companies whose stocks they are buying, and not

just wait for cues and pronouncements from government. It can be a case where

as government intervenes more, it creates more panic and price volatility.

5 Central planning and central disappointment. Central

planning cannot and will not cure and control everything, including stock price

ups and downs, boom and bust. Central planning works mainly to postpone small

busts to become huge busts and bursts. Authoritarianism can never be compatible

with free markets.

6 Role of government. The state and its various agencies,

from local governments to different regulatory agencies to monetary authorities,

should focus on ensuring fair market rules rather than guaranteeing outcomes.

Bienvenido S.

Oplas, Jr. heads a free market think tank in Manila, Minimal Government

Thinkers, Inc., and is also a fellow of South East Asia Network for Development

(SEANET), a regional center based in Kuala Lumpur advocating economic freedom

in the region.

--------------

See also:

BWorld 8, Manila's Traffic and Transport Woes, June 27, 215

BWorld 9, Poitical populism vs. tax realism, July 05, 2015

BWorld 10, Greece crisis, pension and rule of law, July 11, 2015

China Watch 15: FTA, ASEAN and UNCLOS, August 01, 2011

China Watch 19: The Asian Infrastructure Investment Bank (AIIB), October 25, 2014

China Watch 19: The Asian Infrastructure Investment Bank (AIIB), October 25, 2014

No comments:

Post a Comment