----------

Another proposal, raised by Prof. Winnie Monsod, is to

have the Malampaya gas revenue sharing where the government and Shell/private

developers get a 60-40 percent of the gross profit, respectively, be applied to

mining too.

There are several considerations, theoretical and empirical,

in deciding whether to raise, retain or cut taxes in metallic mining, or any

other sectors in general. Here are some.

One, there is a limit to raising taxes. There is an “optimal”

tax rate where government tax revenues can be larger than if government will

further touch the “maximum” tax rate. As the tax goes higher, either people

will reduce working and hence, gross output will decline, or people will resort

to under-report actual production. And government (national and local) tax

assessors and collectors will be happy to accommodate such under-reporting in

exchange for a bribe. This situation is demonstrated by the Laffer Curve.

Figure 1. Optimal

tax rate in the Laffer Curve

This curve is saying that government tax revenue is

larger if the tax rate is only on that “revenue maximizing point” (RMP) rather

than go for 50 or 80 or 100 percent. At higher tax rates, under-reporting of

production, if not under-working, is likely to happen, so that the tax base

declines and hence, revenue collection declines.

Two, there are “deadweight losses” to society as the tax

rates go up. Deadweight loss is an economic term that means “excess burden” or

“inefficiency in resource allocation” because of monopolistic pricing including

government higher tax imposition, externalities and price controls. For

instance, people will buy only a few units of a particular commodity even if

they actually needed more, because of its high price. Or people will buy more

than what they need and end up wasting or losing the excess units bought,

because of government subsidy that result in artificially low price. Such non-

or reduced purchase of certain essential items, or over-purchase of certain

items resulting in wastes, are called excess or unnecessary burden, or simply

“deadweight loss.”

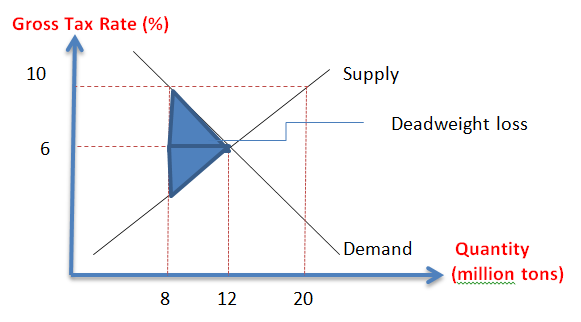

In this hypothetical graph that this author has

developed, let us assume that corporate income tax + excise tax + royalty tax +

certain other taxes would be equivalent to about six percent of the gross

revenues of large-scale mining companies, and consider it as a temporary

equilibrium tax rate . Mining output at that rate is 12 million tons, composite

for various types of metals.

If the government will raise it to 10 percent or higher

to collect more tax revenues, it can result in an area on the left of the RMP of

the Laffer curve and hence, result in higher revenues, or it could be on the right

side of RMP and hence, result in lower revenues.

Figure 2. Possible

Effects of Higher Tax Rate in Mining

A decline in reported production from 12 to 8 million

tons is possible if (a) existing local mining companies will reduce production even

temporarily due to lower international prices of certain metals while local

costs (wages, mandatory social contributions, electricity, fuel, taxes, fees,

etc.) are rising. Or (b) simple under-reporting of actual production by some

companies.

Currently, large scale metalling mining companies (LSMM)

are already paying high taxes and fees to both national and local governments.

In 2010 for instance, LSMM companies paid 43 percent of their net revenue to

the government.

Figure 3. Taxes

and Fees Collection from Philippine Mining, 2010

Source: Dr. Artemio Disini, COMP, presentation at the

Philippine Economic Society (PES) Conference, November 27, 2012, PICC, Manila.

The numbers above would imply that there may be no need

to amend RA 7942, especially on the taxation aspect. But since many sectors and

legislators are driven by the politics of envy, a hike in mining tax may be

inevitable.

The bigger issue in the mining industry is not raising

the tax, but implementing the rule of law. That mining enterprises, large- or small-scale,

local or foreign, should pay the established tax rates and regulatory fees;

that environmental rehabilitation is strictly implemented after a mined out

area; that mine tailings are securely impounded and isolated away from creeks,

rivers, lakes and the sea; that certain community development projects are

implemented to the host villages or barangays of the mining companies.

See also:

Mining 28: Markets, Government and Rule of Law, July 31, 2013

Mining 29: On Open Pit Extraction, Tampakan and SDMP, August 06, 2013

No comments:

Post a Comment